A personal pension is a retirement savings plan in which you make contributions either on a regular basis or a once off lump sum. These contributions are then invested, for example in the stock market, with the aim of building up your pension pot so you have an income when you retire.

A Personal Retirement Savings Plan (PRSA) is another type of PPP. It is like an investment account that you use to save for your retirement. The money paid into a PRSA is tax deductible within certain limits. Unlike a PPP you do not have to be earning an income and paying tax to take out a PRSA.

If employers do not offer an occupational pension scheme or if certain limits apply to their scheme, by law they must offer their employees access to at least one Standard PRSA. Contributions can be made to your PRSA by:

you

your employer only, or

you and your employer

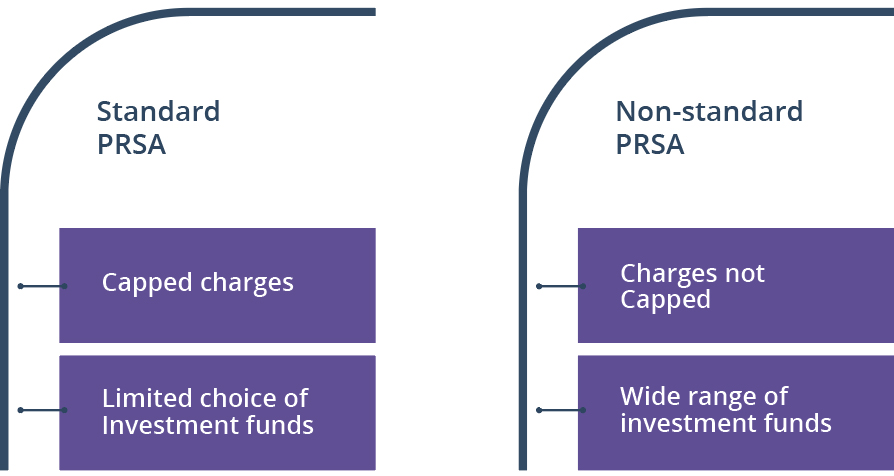

There are two types of PRSAs in the market, a standard PRSA and a non-standard PRSAs. There are two main differences between the two types:

All PRSAs are regulated by the Pensions Authority. Visit The Pensions Authority website for more information on PRSAs.

What age can you retire or take the benefits from your PRSA fund?

The options available to you at retirement are the same as those for Personal Pension Plan (PPP). Information on PPPs can be found at the bottom of this page.

Personal Pension Plan (PPP)

Who can take out a PPP?

A PPP can be taken out by:

Someone who is self-employed

Employees who cannot access an occupational pension scheme.

To take out a PPP you will have to be earning an income which is taxable in the current tax year.

Where can you take out a PPP?

PPPs are provided by insurance companies. You can buy them directly or through banks and brokers/financial advisers.

There are many PPPs on the market and choosing one that suits you can be difficult. Here are some things to think about when choosing a PPP:

Shop around to give yourself the widest choice and take your time to get as much information as you can before you decide.

Make sure you get and carefully read the Disclosure Notice document (sometimes called a Key Features Document). This document sets out all the important facts about the PPP. This must be given to you by the insurance company or broker before you sign into a PPP.

Make sure you can afford the contributions as some PPPs have a minimum payment.

Check what charges you will have to pay, and when. Examples of some of the charges are set up, allocation rate, bid/offer, fund management, fund switching etc. Many of the charges will be deducted from your fund and will affect the value of your pension.

Make sure you are happy with how your contributions are going to be invested and that you are happy with the level of risk you are taking.

PPPs can be complicated so it is recommended that you get independent financial advice. More information on getting financial advice can be found here

Do not sign any documentation until you understand and are happy with your choice.

How much will it cost?

All PPPs will have various charges and they will be set out in your Disclosure Notice document. The following are some of the charges that you may have to pay at the start and during the life of your PPP.

Name of the charge

Explanation

Setup

This charge is to set up the PPP and will be taken from your regular payments. It is typically taken for 6 months to one year but you will need to refer to your disclosure notice document to check this.

Allocation rate

The percentage of your payment that is used to buy units in a fund. A 98% allocation rate means that for every €100 you invest, the insurance company invests €98 and takes €2 as a charge.

Bid/offer spread

The difference between the price to buy and sell units in a fund. If the difference is 5%, it means that €5 out of every €100 used to buy units is taken off as a charge. As a result, the value of a €100 investment would fall to €95. This charge is a feature of older Contracts from before 2005.

Fund Management

This is a set percentage of the value of your investment fund that is taken by the provider each year to pay for managing the fund and other general costs. It typically ranges from 1% to 1.5% of the value of your fund.

Early encashment

This is a fee you may be charged for any money you withdraw in the first few years. This charge is highest for withdrawals in the first year and reduces every year after that. Generally, there will be no charges after five years.

Fund switching

Some PPPs charge a fee if you decide to switch units from one fund to another.

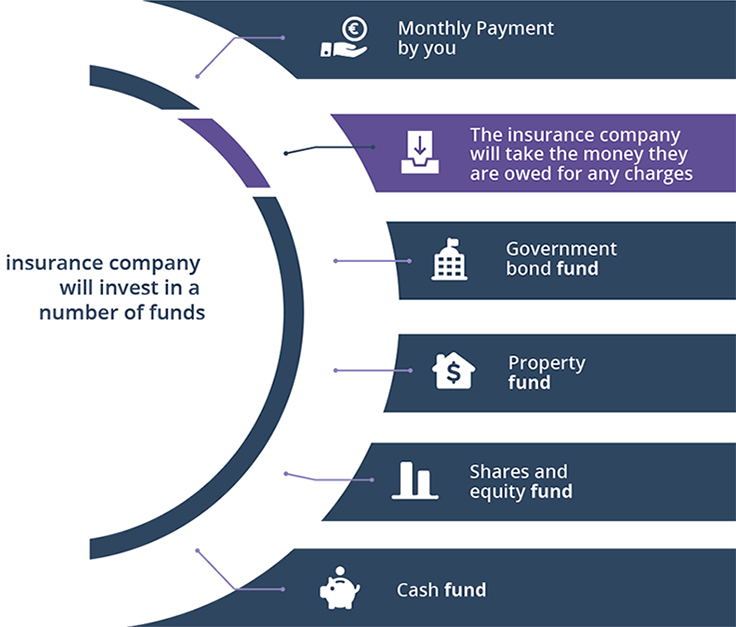

What happens to the money you pay into your PPP?

The insurance company will invest your money in a fund or a number of funds that they feel will perform best to make as much money as possible for you over the life of the PPP. The diagram below shows the type of funds that an insurance company could invest in on your behalf, for example, buying shares in different companies, buying government bonds and investing in property. The insurance company will also take the money for various charges from your contributions.

Top Tip

Investing in funds does not guarantee a positive return and you may not get back all the money you put in.

How to boost your pension

If you think that your projected pension fund may not be enough to meet your needs and wants in retirement, you should look at ways to boost your pension. If you have a PRSA or a PPP, you can increase your contributions. For example, you could consider contributing any increases in your salary to your existing pension.

If you can afford it, you should try maxing your contributions to avail of the maximum tax relief available to you. Learn more about tax relief on pensions.

What age can you retire or take the benefits?

When you retire and if your PPP has performed well you will have a lump sum built up in your PPP fund. This lump sum will be a combination of your monthly payments and any growth that was made from investing your money in various funds, less charges. If during the life of the PPP the investment of your money in various funds did not make any growth, you could have less money than you paid in.

You can take your money from your pension fund in the following circumstances:

from the age of 60 and up to age 75. You do not have to retire or give up work to get the benefits from your PPP. Simply be over 60 and under 70, or,

at any age in the case of serious ill health – this is usually where you are permanently unable to work again, or,

age 50 if your occupation is one where people normally retire before the age of 60 for example a golfer, rugby player, jockey etc.

Top Tip

If you die before taking your benefits from your PPP fund, the value must be paid into your estate.

When taking benefits from your PPP fund you will always have the option of taking a tax free lump sum of 25% (up to a maximum of €200,000). You then have multiple options with the remainder of the balance, if any.

Pat is 64 and is due to retire in a couple of weeks and is looking to take the benefits from his PPP fund. The balance in his PPP pot is €150,000. Pat has a secured income of €14,000 from an employer pension from a job he had a number of years ago. He can take 25% tax free which is €37,500. The balance of €112,500 can be invested in an Approved Retirement Fund (ARF), an annuity or he can take it as a taxable lump sum.

Joan, 65

Joan is 65 and has just retired and wants to take her benefits from her PPP fund. The balance in her PPP fund is €25,000. She can take 25% tax free which is €6,250. She does not have any other income. The balance of €18,750 can be invested in an Approved Retirement Fund (ARF), an annuity or she can take it as a taxable lump sum.

Post retirement products

What is an Annuity?

An Annuity is a long term investment that is sold by insurance companies. You give the insurance company a lump sum from your pension fund and in return the insurance company will guarantee to pay you an income for the rest of your life – you will have to pay tax on this income.

You do not have to buy an Annuity from the same insurance company that you bought your PPP from so you can shop around in order to get the best return on your lump sum. There is a maximum guarantee period of 10 years on annuities which are bought from the money in your pension fund. The guarantee period is the number of years the insurance company will pay out an income to your estate if you die shortly after taking out the annuity.

Example

Tim

Tim has just retired and has €200,000 from his PPP fund to invest/buy an annuity. After talking to a number of insurance companies, the best offer he got was an income of €8,000 per year with a guaranteed period for the first 5 years.

After 2 years, Tim dies – the insurance company will continue to pay €8,000 per year for the next 3 years into Tim’s estate.

What is an Approved Retirement Fund (ARF)

An ARF is an investment plan that allows you to continue to invest some or all of the benefits from your pension fund in retirement and take out money as you need it, rather than buying an annuity. However, you must take at least 4% per year of the value of the ARF up to age 70 and after that at least 5% per year.

Can you transfer your PPP to another pension plan?

PPPs bought since 6 April 1999 can be transferred to another PPP. They can also be transferred to a Personal Retirement Savings Account (PRSA), but only if the provider operating the PPP allows for it.

What information should you get from your insurance company/broker?

Disclosure Notice

A disclosure notice must be given to you before you sign a PPP application form. This document is to help you decide if the PPP is suitable for your needs and includes information such as

the likely changes that might be made to the plan

the likely charges payable to the insurance company

the likely benefits the PPP might provide to you at retirement.

When you are taking out a PPP and a general disclosure notice is provided, it will include a personalised table of likely benefits and charges. In addition, the personalised table should outline that you have a cooling off period of 30 days from the date you received your PPP policy or the date the insurance company posts it out to you.

Annual statement of value

For PPPs taken out after 1 February 2001, insurance companies must give you an annual statement which shows:

The current premium payable

The current surrender or maturity value

And any other information the insurance company thinks is necessary

12 June 2023

Pensions

How can I retire early?

Should I transfer an old pension into my current one?

Will I be automatically enrolled in a pension?

What is the best pension if you're self employed?

Is it too late to start a pension at 58?

If you’re self-employed and wondering what your best options are, read our information on personal pensions. You may have recently taken up employment and are unsure if you’re paying an employee pension.

A visitor to the money clinic wanted to know if he should he transfer an old pension into his current one. Eoin offers some expert advice on what to do.